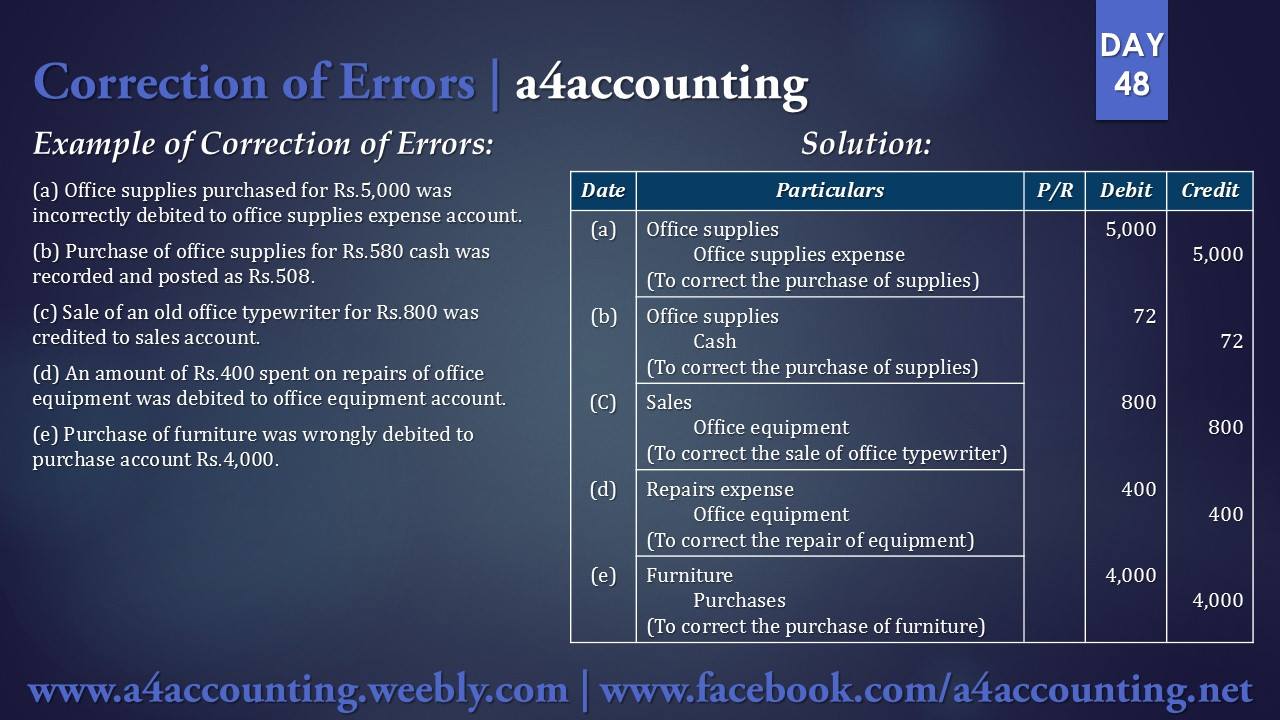

(a) Purchase of supplies was wrongly debited to supplies expense account Rs.5,000.

Step # 1: What was the double entry?Office supplies expense 5,000 Dr. and Cash 5,000 Cr.

Step # 2: What should the double entry have been?

Office supplies 5,000 Dr. and Cash 5,000 Cr.

Office supplies 5,000 Dr. and Cash 5,000 Cr.

Step # 3: Correcting entry:

Office supplies 5,000 Dr. and office supplies expense 5,000 Cr.

Office supplies 5,000 Dr. and office supplies expense 5,000 Cr.

(b) Purchase of supplies for cash Rs.580 was recorded as Rs.508.

Step # 1: What was the double entry?

Office supplies 508 Dr. and Cash 508 Cr.

Step # 1: What was the double entry?

Office supplies 508 Dr. and Cash 508 Cr.

Step # 2: What should the double entry have been?

Office supplies 580 Dr. and Cash 580 Cr.

Office supplies 580 Dr. and Cash 580 Cr.

Step # 3: Correcting entry:

Office supplies 72 Dr. and cash 72Cr.

Office supplies 72 Dr. and cash 72Cr.

(c) Sales of typewriter credited to sales account Rs.800.

Step # 1: What was the double entry?

Cash 800 Dr. and Sales 800 Cr.

Step # 1: What was the double entry?

Cash 800 Dr. and Sales 800 Cr.

Step # 2: What should the double entry have been?

Cash 800 Dr. and Office equipment 800 Cr.

Cash 800 Dr. and Office equipment 800 Cr.

Step # 3: Correcting entry:

Sales 800 Dr. and Office equipment 800 Cr.

Sales 800 Dr. and Office equipment 800 Cr.

(d) Repair of equipment was debited to equipment account Rs.400.

Step # 1: What was the double entry?

Office equipment 400 Dr. and Cash 400 Cr.

Step # 1: What was the double entry?

Office equipment 400 Dr. and Cash 400 Cr.

Step # 2: What should the double entry have been?

Repairs expense 400 Dr. and Cash 400 Cr.

Repairs expense 400 Dr. and Cash 400 Cr.

Step # 3: Correcting entry:

Repairs expense 400 Dr. and Equipment 400 Cr.

Repairs expense 400 Dr. and Equipment 400 Cr.

(e) Purchase of furniture debited to purchase account Rs.4,000.

Step # 1: What was the double entry?

Purchases 4,000 Dr. and Cash 4,000 Cr.

Step # 1: What was the double entry?

Purchases 4,000 Dr. and Cash 4,000 Cr.

Step # 2: What should the double entry have been?

Furniture 4,000 Dr. and Cash 4,000 Cr.

Furniture 4,000 Dr. and Cash 4,000 Cr.

Step # 3: Correcting entry:

Furniture 4,000 Dr. and Purchases 4,000 Cr.

Furniture 4,000 Dr. and Purchases 4,000 Cr.

Comments

Post a Comment